Relevant Cost of Material

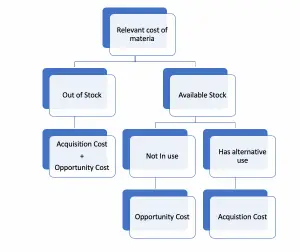

Relevant Cost of material is the incremental cost of raw material, which will change depending on the production quantity. It is an additional avoidable cost, which only occurs when the specific decision is made. We only need the material when we decide to process the production. So the management will consider between accept or reject the order.

Relevant cost is the analyze of production cost by comparing between the current contribution and new contribution if company accept the order. The company want to maximize the profit, so we need to analyze if new order bring more profit to company.

Rule of Relevant Cost

Out of stock

If the material is not available in stock, the relevant cost will be the acquisition cost at the current market price. Some material can produce internally, so we may include the opportunity cost, which raises from the production.

- In stock but has an alternative use

The relevant cost will be the market price plus any transportation cost which brings the material to use.

- In stock but not in use

If the material is available but not in regular usage, the relevant cost will be the higher of:

- Scrape value and

- Its alternative usage

Example of relevant cost of material

Company A is considering a new order which requires 50,000 units of product X, which sale at $ 200 per unit. Based on the production manager, Prodcut X require 3 materials to produce with the following detail:

| Material 1 | Material 2 | Material 3 | |

|---|---|---|---|

| Material required per unit of product X | 5 Kg | 2Kg | 1Kg |

| Available in stock | 0 | 200,000 Kg | 50,000 Kg |

| In use? | No | No | Yes |

| Market price per Kg | $ 20 | $ 15 | $ 30 |

| Scrap value | $ 8 | $ 5 | $ 10 |

Assume the suppliers will deliver all material to our warehouse without further charge.

Calculate the relevant cost of all material.

- Material 1

The material is not in our stock, so we have to buy from suppliers if we want to accept this order.

Relevant cost of material 1 = 50,000 units * 5Kg * $ 20 = $ 5,000,000

- Material 2

The material is available but it does not have any alternative use, so its relevant cost is the scrap value. It only brings value by scarping.

Relevant Cost of material 2 = 50,000 units * 2Kg * $ 5 = $ 500,000

- Material 3

The material is available but also for other products, so we have to purchase them from the market.

Relevant cost of material 3 = 50,000 * 1Kg * $ 30 = $ 1,500,000

Total relevant cost of all material = 5,000,0000 + 500,000 + 1,500,000 = $ 7,000,000

Increase in contribution = (50,000 units * $200) – 7,000,000 = $ 3,000,000

So the company should accept this order as it will increase the contribution of $ 3,000,000 compare to current contribution.