Life Cycle Costing

Life cycle costing is the costing method that includes all costs over a product life cycle. We estimate the total product revenue and costs in its lifespan in order to make a decision. The company wants to make a profit in the long-term not only one or two years, so tracking the profit of each product is very important. As some products may provide profit only in one or two years while requiring a huge investment in R&D and restoration cost.

Life cycle costing will calculate the costs and revenue per product lifes cycle, so the top management can make a precise decision to ensure company long-term profit. The cost will include everything from research and development (R&D), production cost, and cost of discontinuing production.

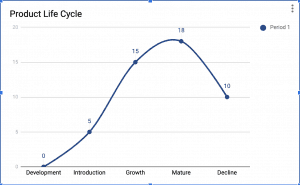

Product Life Cycle Graph

Development

It is the stage when the company does market research on a new product, it focuses on customer needs, requirements, and competitors’ feature. After that, we will develop and design a new product to fit in the market. Up to this point, there is no revenue yet, only the cost that incurs.

Introduction

It is the time when the company injects the new product into the market. There will be a huge marketing campaign to promote and advertise to the target customers. It may be some revenue with a very high marketing expense during this time.

Growth

After some time, the sale will start to increase, and the marketing expense will begin to decrease as the customers already aware of our product. It is the time that sale starts to generate, and the product begins to make a profit.

Mature

The product’s demand will not increase anymore and it reaches the peak period. It is a time when most sales are made with the most profitable period. The company will try to extend this period as long as possible to maximize the profit.

Decline

Sooner or later, the demand will be declined as the features are outdated, new substitute products, or a better choice from the competitors. The profit will start to decrease, or It doesn’t make any more profit. The company has to decide to continue or stop production.

What are the costs that included in the life cycle costing?

| Costs that included in the life cycle costing | |

|---|---|

| Research and design cost | Even though the company does not make a sale, but we need to cover all costs since the beginning. It will consist of survey cost, product test, production of sample product and so on. |

| Marketing and Advertising cost | It will be huge in the introduction stage and decrease afterward, but some products require ongoing advertisement. All of them must include life cycle costing. |

| Training Cost | It is the cost that company spend to train worker to produce new product. |

| Production Cost | It is the cost associated with the production, such as direct material, direct labor, and overhead. |

| Cost of disposal | Some products require the company to restore the production site after the product’s life, such as cleaning and restore the environmental impact. |

Why do we need to use life cycle costing?

Life cycle costing will be used in the design stage, when we decide to start the design of this new product. So most of the figures are the budget which we receive from various sources such as market research, past experience, and industry information.

It is the time when management has to decide to make this product or not. Managements may have a few products to be selected for investment. They will choose the highest profitable product.

Looking at the full life product helps us to see the full picture rather than one or two year profit which could be misleading.

What are the Advantages of Life Cycle Costing?

| Advantages of Life Cycle Costing | |

|---|---|

| Full budget over the product life | Management will be able to look at the full budget, which covers the lifetime of the product; all expenses and revenues are included. |

| More accurate cost per unit | While all the expenses since R&D up to the restoring cost include in the product, the profit per product will be more realistic than the traditional method. |

| Select the highest profitable product | Life cycle costing will enable the company to select the most profitable product to be made. It will help to maximize shareholder wealth as well as management performance. It also enables comparison from one product to another. The comparison annual profit is not enough because it ignores the R&D cost as well as the contingent cost that will occur after product life. |

| Redesign the product | Management may want to decrease the product cost when the life profit is too low. We can ask the engineer to redesign the product by withdrawing some feature to reduce cost. We can do this in the early stage when products are not mass-produced. On the other hand, management may redesign the product by adding new features to extend the product life, which will maximize the profit as well. |

| Encourage management to have a long term view | This method will enable the management to focus on the long term future of the company rather than meet short term targets and get high bonuses. |

| Involve the contingency liability | Contingent liabilities are most likely to ignore by other method besides the life cycle costing. It is a massive expense for the company. We are responsible for restoring the original state of the environment. |

What are the Disadvantages of Life Cycle Costing?

| Disadvantages of Life Cycle Costing | |

|---|---|

| Estimate only | This method relies heavily on the estimation of revenue that receives from market research and past experience. If anything wrong with this sale figure, the whole system will not work. The product will not making any profit for the company. |

| Not flexible when market change | We expects the market to precisely the same as our product develop, produce, and sell to the market. But everything changes from time to time, and it will impact our product life.Due to the trending, customers may need different products by the time we reach the market.

Our product’s life may be shorter as the competitor keeps inject a similar or better product to the market. With all these changes, the actual situation will be different from our expectations, and it will impact our strategic plan. |